Summary

- Even despite Cathie's $3,000 price target, we think that Tesla is overhyped and overvalued.

- Most individual investors would do much better if they stuck to simple and boring businesses that they can truly understand.

- We present two such investment opportunities that we currently hold in our portfolio.

- Looking for a portfolio of ideas like this one? Members of High Yield Landlord get exclusive access to our model portfolio.Learn More »

Recently, the bigheadlineon Seeking Alpha was thatARK Invest's Cathie Wood (ARKK) fired off a $3,000 price target onTesla(TSLA):

The news generated a lot of interest as can be seen in the 849 comments!

The current share price is $610, so this means that Tesla has 392% upside potential according to this estimate.

But how realistic is this really?

Tesla has already risen by 500% over the past year...

It is already a massive company with a $600 billion market cap...

It trades at over 100x earnings even based on highly optimistic expectations...

And perhaps the most disturbing part is that its main business is cars, which is arguably one of the worst businesses there is:

- Low margin

- Capital intensive

- Very cyclical

- High recurrent capex

- Extremely competitive

To give credit where it is due, Tesla is an innovator and it has had great success so far. But now, competitors are coming for their piece of the pie and doubling down on their efforts to produce and sell electric vehicles that directly compete with Tesla.

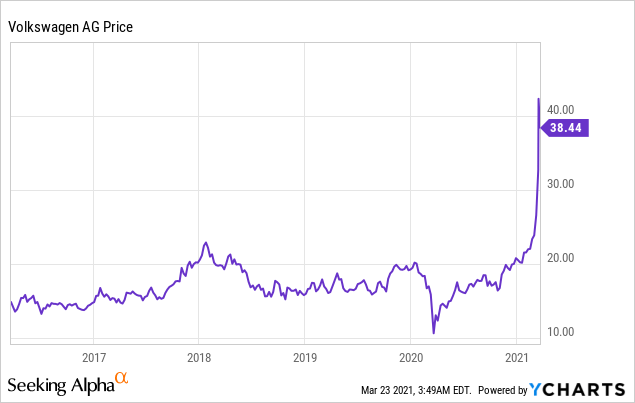

Before you discredit the competition, just take a look atVolkswagen's (OTCPK:VWAGY) share price as it moves to take over some of Tesla's business:

If Tesla struggled to turn a profit with close to no competition, how will it perform once all major car manufacturers begin to seriously scale their electric car businesses?

Soon, it will be much cooler to have a brand-new electric Audi than buying a Tesla, which is getting boring in comparison. Teslas are everywhere already and it is not what will set you apart:

I can't help but think that Cathie's $3,000 price tagunderestimatesthe impact of rising competition:

"In ARK's view, companies with 'old world DNA' are unlikely to transition quickly enough to dominate the new world. Often the difference between old and new world DNA are plans for linear as opposed to exponential growth trajectories. Tesla's stated goal for 2030 is three terawatt-hours of annual production, 12.5 times more than VW's 240 gigawatt-hours. In an exponential world, companies thinking linearly could be left behind."

Call me "old-world", but that makes little sense to me.

I think that Volkswagen is much more capable and efficient than they make it seem to be, and Volkswagen is just one company among many others that are moving into this space.

The bottom line is that Tesla is a car company. We hate car businesses. And we hate even more its current valuation and future business prospects.(I get that Tesla isn't just about cars, but its other segments are not profitable and very small in comparison).

With so many question marks about Tesla's future, we see Tesla's stock as highly speculative at best, and outright dangerous at worst.

Tesla is exciting... but speculating with Tesla-type stocks rarely ends well for individual investors. We think that most investors would do much better if they just focused on boring investments instead.

Good investing should be boring, not exciting, and there is nothing wrong with earning steady 8-12% annual returns from defensive investments.

Forget Tesla, buy these boring high-yielding stocks instead:

Boardwalk (OTCPK:BOWFF)

Apartment communities are some of my favorite investments because:

- They are very simple to understand.

- They generate defensive income from rents.

- They provide steady growth and inflation protection.

It does not get more boring than this, but that's a good thing in my book.

You buy the property. You get a cheap mortgage. And then you rent it out and let your tenants pay off your mortgage, all while you earn steady income and wait for the property to appreciate.

The only downside is that the management of apartment communities can be time-consuming and stressful. You don't want your investment to turn into a part-time job, which is often the case when you start to deal with tenants.

That's one of the many reasons why we like apartment REITs.

They allow us to invest in apartment communities and enjoy their returns without actually having to do any of the operational work. Moreover, we also enjoy better liquidity, low transaction cost, diversification, and professional management, all of which, improve the risk-adjusted returns.

Unfortunately, in today's market, most apartment REITs are quite popular and trade at close to fair value. Companies like Essex Property (ESS), Equity Residential (EQR), and Mid-America (MAA) may prove to be attractive long-term investments, but they are priced at ~20x cash flow, which isn't particularly cheap when you consider that they are suffering from the pandemic.

We think that better opportunities are today in smaller and lesser-known apartment REITs, particularly in foreign markets.

Currently, one of our favorite opportunities isBoardwalk REIT, which is a small Canadian apartment REIT with a well-diversified portfolio of Class B affordable apartment communities:

The nice thing about BOWFF is that because it specializes in affordable apartment communities, its income is very resilient. Affordable housing is always needed, and especially so during times of crisis when people cut back on spending.

Moreover, BOWFF's current rents are 10-20% below market and the management is able to unlock value and hike rents by doing minor cosmetic fixes to its properties. Here is an example in which they renovated the community room at Spruce Gardens in Calgary:

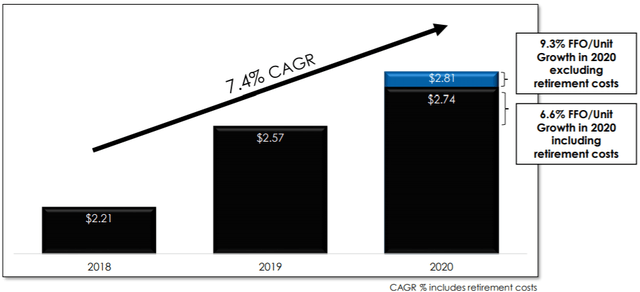

These small esthetic improvements make a big difference when leasing apartments to new tenants, and we saw that in 2020 as they managed to grow rents even despite the pandemic:

- 3.7% same property NOI growth.

- 6.6% FFO per share growth.

- 9.3% FFO per share growth, excluding one-time retirement costs.

These results are better than 99% of apartment REITs.

Based on that you would expect it to trade at a premium valuation, but it is actually the opposite:

BOWFF is today priced at just 13x FFO and a 40% discount to estimated NAV, which is much cheaper than most other apartment REITs.

We estimate that the company has 50% upside potential, and while you wait earn steady cash flow from the properties. The cash flow yield is nearly 8% at today's price, and BOWFF pays out 3% of that in dividends and reinvests the other 5% in growing its business.

That's very attractive for a defensive apartment REIT investment.

VICI Properties (VICI)

VICI Propertiesis a net lease REIT, which is one of our property sectors at High Yield Landlord.

In case you are not familiar with net lease properties, they are single-tenant freestanding properties that serve as profit centers to their tenants. Good examples include McDonald's (MCD) restaurants, Dollar General (DG) convenience stores, 7/11 gas stations, etc.

What makes these properties so attractive is that their leases are generally very favorable to the landlord. That's why we call them "net leases":

- The lease term is generally very long at 10-15 years.

- The rent is automatically increased by 1-2% each year.

- And most importantly, the tenant pays all property expenses, incl. repairs.

Illustrative picture of a Walgreens (WBA) net lease property:

As such, these properties are resilient to recessions, and net lease REITs are able to pay steadily rising dividends even when times get tough.

In fact, during the pandemic, most of these REITs hiked their dividends.

But none of them hiked it by as much as VICI Properties, which really made a statement by hiking it by 11% in the midst of the crisis.

What's unique about VICI is that unlike most other net lease REITs, it specializes in only net leased Casinos. This has many advantages as highlighted in the table below:

| Casino Net Lease Property | Regular Net Lease Property | |

| Cap rate | 7-9% | 5-7% |

| Rent escalations | 1.5-2% | 1-1.5% |

| Lease Length | 15 + 5 | 10-15 + 5 |

| Normalized Rent Coverage | 3-4x | 2-3x |

| Occupancy Rate | 100% | 98-99% |

| NOI Margin | 95-100% | 90-95% |

| Capex Need | Very low | Low |

| Barrier-to-Entry | High | Low |

| Lease Renewal Likelihood | Very high | High |

| Technology Risk | Below average | Depends |

| Master Lease Protection | Yes | Occasional |

| Mission Critical Real Estate | Yes | Yes, but to a lesser extent |

| Lease expiration in next 5 years | 0% for VICI | 3-5% per year on average |

| Competition for Investments | Low | High |

| Investment Spreads | Above average | Average |

| Iconic Assets | Some | No |

Source: author

During the crisis, all its tenants kept paying their rent in full and on time because these properties are absolutely essential to their businesses. Moreover, because the rent coverage ratios were high prior to the pandemic, there was enough margin of safety for its tenants to survive the storm.

So while others were playing defense, VICI kept on acquiring new properties in 2020, which led to rapid cash flow growth.

And it isn't stopping here. Just recently, VICIannouncedthat it is acquiring the Venetian in Las Vegas in a massive $4 billion transaction:

This acquisition will be immediately accretive to FFO per share, and greatly improve the average quality of VICI's portfolio.

Given how it has started the year, we think that 2021 will be another year of rapid growth, with a large dividend increase coming in the second half of the year.

Despite that, VICI is today priced at just 14x FFO, which is unreasonably low when compared to the multiples of its close peers. As an example Realty Income (O) is priced at 19x FFO despite growing at a much slower pace and experiencing greater difficulties during the pandemic.

We expect VICI to reprice at closer to 18x FFO, which will unlock 30% upside, and while you wait, you earn a rapidly rising 4.8% dividend yield.

Bottom Line

Tesla is exciting, but it is also priced at an extreme valuation and its future is very uncertain. In many ways, this situation reminds us of the dot-com bubble and the following crash.

Will Tesla pay off in the long run? Maybe, but it sure feels a lot more like speculation than investing at this point.

We think that most individual investors would be much better off if they stuck to simple and boring businesses that generate steady and predictable cash flow.

BOWFF and VICI are two good examples of that, but there are many others. At High Yield Landlord, we currently invest in 23 similar REITs that generate us an average ~10% cash flow yield while we wait patiently for long-term appreciation. Good investing should be boring, not exciting, and next to Tesla, these are very boring investments.

Comments