Summary

- Fintech company SoFi is the newest kid on Wall Street after coming public through a SPAC merger with Social Capital Hedosophia Holdings Corp. V in early June.

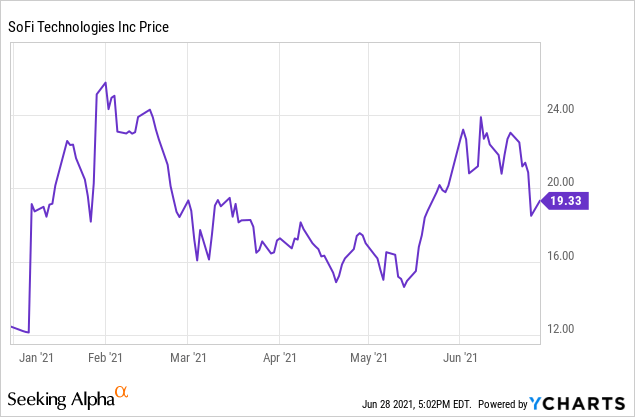

- The stock is still very much in price discovery mode and shares remain volatile as they dropped around 15% during the past 3 trading days.

- With a forecasted 43% topline CAGR until 2025, SoFi has one of the strongest growth prospects in the fintech industry, led by its Banking-as-a-service and financial services segments.

- We believe SoFi can meet or even exceed its forecasted CAGR which should move the company‘s valuation closer to between $30 to $40bn until 2025.

- We illustrate possible valuation scenarios for 2025 below.

Summary

SoFi Technologies (SOFI) hit the public markets through a SPAC merger with Social Capital Hedosophia Holdings Corp. V led by famous financier Chamath Palihapitiya. There isn’t much information coming from SoFi‘s charts so far as the stock just went public under the ticker SOFI in early June and is still very much in price discovery mode. Shares havetraded in a range between $15 and $25 for the past months but saw significant declines during the past 3 trading days. Shares are now down almost 15% in a week at the closing price of around $19/share on June 28th, but shares were actually down to a multi-week intraday low of $17.65 / share. Currently, SoFi trades at a valuation of around $15 billion based on 800 million shares outstanding as of this writing.

Investors should be aware that much of the recent declines can be attributed to a big lock-up expiration that commenced on Monday, 28th June.

Lock-up expirations generally put pressure on a stock for the short-term, especially as early-stage shareholders are finally allowed to offload shares on the public markets. It is interesting to see that Rosenblatt Securities’ analyst Sean Horgan put a $30 price target on SoFi and reiterated that the short-term term headwinds create a potential long-term buying opportunity:

We see a unique buying opportunity as a result of this recent selling and ahead of a potentially significant upside catalyst (bank charter approval). Pressure from early investors taking profits (and short-selling ahead of the lock-up expiration) are likely to weigh on the stock in the near term. However, we expect SOFI's bank charter approval process to conclude before year-end (adding >25% upside to our EBITDA estimates).

We could not agree more. As much as SoFi stock has been trending downwards, the underlying company is showing all signs of a robust business with strong growth prospects. In fact, we believe that at a current valuation of $15bn, SoFi could grow into a much larger valuation of around $30 to $40 billion until 2025, if not higher, based on our modelling: the following assumptions:

- SoFi can generate at least $5bn in revenues by 2025, supported by a bank charter.

- This boosts incremental revenues until 2025 by $3 to $3.9bn at an average weighted EBIDTA margin of 25,5% for 2021 to 2025.

- We take a more conservative revenue multiple closer towards Square’s (SQ) roughly 8x TTM P/S ratio.

- We apply a 25x EBIDTA multiple in 2025 (for comparison:Square‘s adjusted EBIDTA multiple is >100x at the moment).

Based on this back-of-the-envelope math SoFi could actually exceed the $5bn in total revenue with a bank charter, and based on P/S and adjusted EBIDTA multiples, this gets us to a market cap of around $40bn by 2025 if the bank charter is granted.

But even at the conservative end of the current 2025 revenue guidance of $3.7bn (without a bank charter) and with $1.177bn in adjusted EBIDTA for 2025 and a 25x EBIDTA multiple, the company should be able to get close to a $30bn market cap, implying a double from current levels by 2025, or a 20-25% average annual return in the base case.

What Makes SoFi So Special?

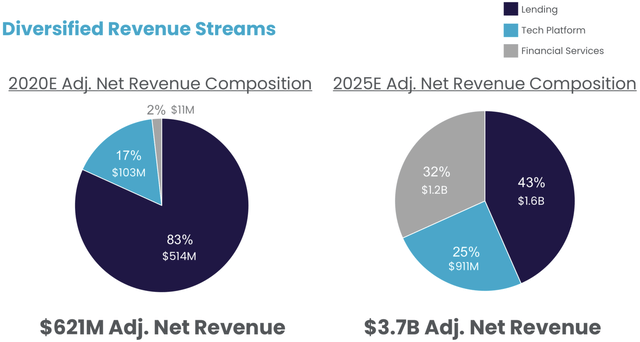

SoFi operates a financial technology platform that generates revenue from3 core segments: Lending, its fintech or banking-as-a-service platform Galileo, and financial services. The product portfolio covers a wide range of services, including personal, student, and home loans, stock and crypto investing, credit card issuing with direct cash back, money management, as well as fintech or Banking-as-a-service through Galileo‘s technology platform.

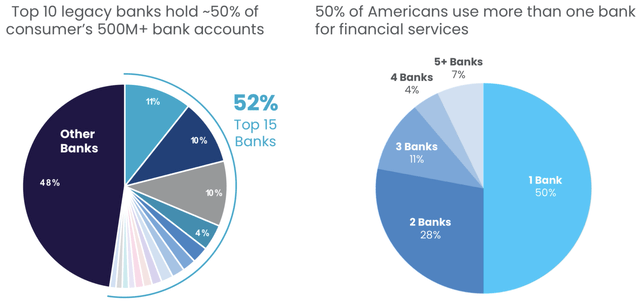

The breadth of SoFi’s offering is really impressive and leaves competition far behind. There is no offering that combines all these services in a standalone app. The SoFi platform is kind of a „super-app“ for all things financial-related as it offers a full suite of financial products. This is a compelling argument by which SoFi should be able to pull a large share of customers from legacy banks, from which the top 10 hold ~50% of consumer’s 500M+ bank accounts in the US. A large pie up for grab especially if you consider that around 50% of Americans use more than 1 bank account to fulfill their needs due to the lack of an integrated financial one-stop shop on a digital platform.

Financial Performance

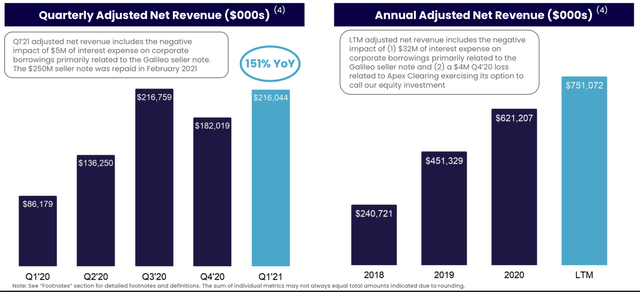

SoFi hit the public markets just about the right time when they reported accelerating growth across its business with a YoY increase in revenue of 151% to $216 million which easily beat management’s guidance of $190-195M with a 11-14% beat.

- SoFi's Lending segment generated $168 million in revenue and accounted for 76% of total revenue in Q1 2021 which was up 106% YoY.

- The Technology Platform segment generated around $46 million in revenue, which includes the fintech solution Galileo, with an astronomical growth rate of >45x compared to just under $1 million in revenue in the year-ago quarter. Revenue from the segment accounted for 21% of total revenue.

- The financial services segment grew revenues by 200% YoY to $6.46 million.

SoFi also reported strong customer growth with the 7th consecutive quarter of YoY growth acceleration in total customers.

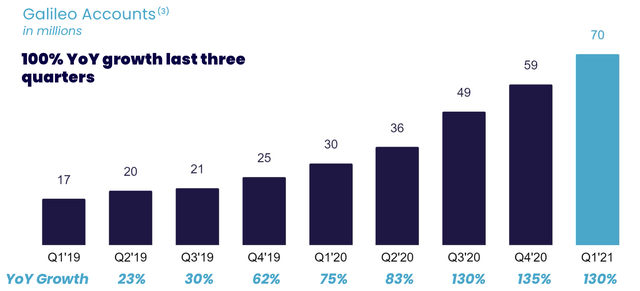

The firm also doubled down on strengthening its technology platform by acquiring the fintech platform Galileo. Galileo is the backbone of almost the entire digital banking market in North America and serves around 70% of the top 100 fintech companies globally. Galileo is expected to be a major revenue driver for SoFi in the long-term. Galileo enables companies to build out their own financial products in payment, card issuing, and digital banking, amongst other functionalities.

The Galileo platform saw the 3rd quarter in a row of 100% YoY customer growth, which is quite impressive. That‘s a significant acceleration from the growth rates that Galileo saw back in 2019. The business combination fits nicely into the overall SoFi strategy of expanding the product portfolio, and with Galileo, SoFi is now also penetrating the business-to-business revenue stream right next to its consumer-facing offerings. The combination will likely also accelerate and expand SoFi’s existing products & services to the 70M Galileo accounts, a nice cross-selling opportunity.

Business Outlook

SoFi also reiterated its previous guidance of $980 million in FY 2021 revenue, representing a 58% YoY growth rate. In the long-term, the company expects to generate $3.7bn in revenues by 2025 - and that‘s without the issuance of a bank charter which the company applied for very recently.

SoFi separates its forecast into the 3 core revenue streams, as shown below. It is apparent that the Galileo technology offering and the financial services will contribute a much larger share of revenue by 2025 as they are expected to grow by a CAGR of 55% and 153% respectively until 2025, while the core lending business is expected to grow at a very robust CAGR of 25% until 2025.

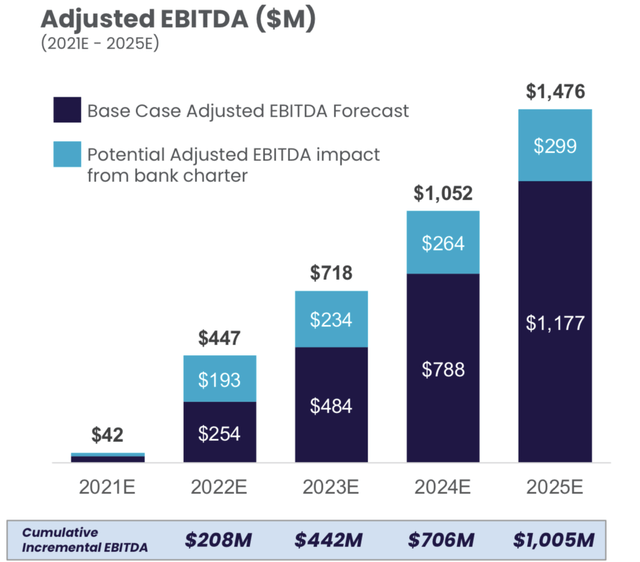

The company also guides for adjusted EBITDA of $1.177 billion by 2025, which would increase to around $1.5 billion with a bank charter, implying a roughly $1bn in additional revenue for 2025 alone from that bank charter at a 32% adjusted EBITDA margin that the company is projecting, or between an incremental $3 to $3.9bn in incremental revenue between 2021 and 2025 (based on author‘s own calculations, see below). The EBIDTA margin may actually be higher due to lower cost of capital with a bank charter, so that the forecasted incremental revenue add from the bank charter would be a bit less, hence the $3 to $3.9bn range.

Assuming a bank charter is granted, we believe that SoFi can hit the $5bn revenue mark by 2025, if not exceed it. It is difficult to find another public company in the fintech space that is growing as quickly as SoFi does. Remember that SoFi grew revenues by 151% in the latest quarter and is forecasting 58% YoY growth for FY2021,and a 43% revenue CAGR until 2025.And that’s all without a bank charter, which would give a nice top-and bottom-line boost based on cheaper borrowing cost by which SoFi would be able to increase the number of loans, reduce operating costs and provide even better product competitiveness.

Valuation Scenarios for 2025

We believe that at a current valuation of $15bn, SoFi could grow into a much larger valuation of around $30 to $40 billion until 2025, if not higher, based on the following assumptions:

- SoFi can generate at least $5bn in revenues by 2025, supported by a bank charter, which could yield an incremental $1bn in EBIDTA by 2025, as forecasted by management.

- This would imply an incremental boost to revenues of around $1bn for 2025 alone at the forecasted 32% EBIDTA margin from SoFi's management, or between $3 to $3.9bn in incremental revenues from 2021 until 2025 at an average weighted EBIDTA margin of 25,5% from 2021 until 2025 (margin is calculated by the incremental EBIDTA add from the bank charter each year multiplied by the % share of incremental EBIDTA of $1bn for each year).

- We assume a re-rating of the revenue multiple closer towards Square’s (SQ) roughly 8x TTM P/S ratio (almost half the current multiple from SoFi) as revenue growth would still be quite strong at 25% to 30% in 2025.

- We apply a 25x EBIDTA multiple in 2025 (for comparison:Square's adjusted EBIDTA multiple is >100x at the moment, so our assumption should be conservative).

Based on this simplified back-of-the-envelope math SoFi could actually exceed the $5bn in revenue with a bank charter, and the company should at least be able to get to a $30bn, if not a $40bn valuation or higher. The assumptions get a bit messy here depending on the multiples you apply, but 8x on TTM sales or 25x on EBIDTA doesn‘t seem to be very overextended, especially if topline growth would still be at around 25 to 30% in 2025 for SoFi.

But even at the conservative end of the current 2025 revenue guidance of $3.7bn (without a bank charter), that SoFi’s management is pulling up, coupled with a TTM P/S multiple of8x, or a 25x EBIDTA multiple the company should be able to get close to a $30bn market cap.

Risks

Obviously, competition is a key risk. SoFi operates in a very competitive industry with established players like PayPal (PYPL) and Square (SQ) as leaders in the field. But also the rise of so-called neobanks should be closely watched. If you look at slide 17 of the IPOE presentation from the SPAC merger, it shows that 296 neobanks have emerged in the last 10 years, which could all become serious competitors to SoFi in all product segments. Names include Stripe, Marqeta (MQ), N26, and many others.

The one thing that should set SoFi apart is the breadth of its technology offering, as it is the only one-stop-shop for all financial-related aspects. Expanding its product offering, e.g. as SoFi recently did with the launch of auto loans, and driving the growth of its fintech backbone Galileo should do its part in keeping that moat. It was reported in that, in 2020, Galileo hat a 95% market share in digital banking in North America with 70 of the top 100 Fintech companies globally using Galileo as the core platform. This alone, together with the recent growth from Galileo (remember the 45.2x growth in Q1 2021 above) clearly illustrates that there is a strong moat.

Another risk to keep in mind is the lock-up expiration that hit the stock on 28th June which could create further short-term downward pressure on the stock as early-stage investors are taking some profits.

Conclusion

In summary, SoFi’s technology platform and breadth of offerings is one of the most compelling in the fintech space. Current numbers, growth prospects and management are exceptionally strong. Following recent stock price declines SoFi trades for around 15 times this year‘s projected revenues of $980 million - not a cheap valuation - but with a view to a potential $5bn in revenues by 2025, supported by a bank charter, the stock doesn’t actually look very overextended to us at these levels, Even at the lower-end of the 2025 revenue guidance of $3.7bn (without a bank charter), coupled with a re-rating of the revenue multiple closer towards 8x TTM P/S ratio (almost half the current multiple), or a 25x EBIDTA multiple, the company should move closer towards a $30bn valuation, which would be a double from current levels by 2025, or a 20-25% average annual return. We agree that the bank charter would be key to further upside on the base scenario, and we believe that SoFi can get there. We have initiated a small long-term position around $19 / share.

Comments