Investment thesis

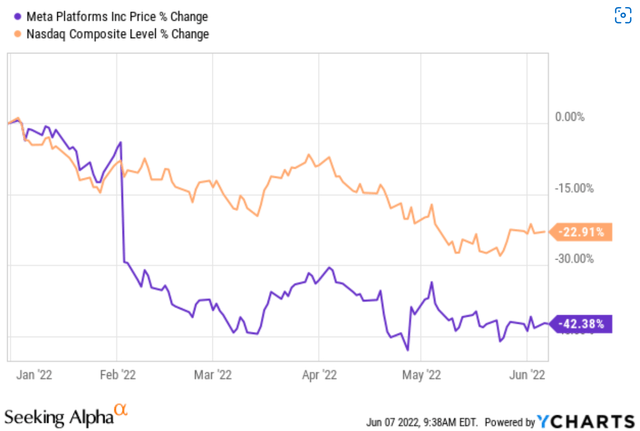

Meta Platforms, Inc. (NASDAQ:FB) is now a growth company priced as a terminally cheap one. Its prices have dropped more than 42% YTD, and valuation contracted from a peak of 28x P/E a few months ago to about 16x FW P/E on a GAAP basis. Such a large correction was driven by a multitude of factors.

First, the NASDAQ composite index itself suffered a correction of more than 22% YTD. Second, many macroeconomic risks are unfolding and keep pressuring equity valuation, including inflation, supply-chain disruptions at advertisers, and also a nonnegligible possibility of a recession. Lastly, specific to FB, it is dealing with slowing rates of user monetization and the privacy changes in Apple’s iOS system

The thesis here is that at the current valuation, all the above negative scenarios have been fully priced in. You will see that FB’s true owners’ earnings have been consistently better than its accounting earnings. Hence, its valuation is even more attractive than on the surface, by about 54% based on a Greenwald analysis to adjust for the growth CAPEX, as discussed immediately below.

Seeking Alpha

FB’s accounting EPS and owners' earnings

The commonly quoted P/E for FB is based on the GAAP accounting earnings. And as of this writing, it varies in the range from 14x to 16.6x depending on whose report your read (e.g., Yahoo Finance or Seeking Alpha) and the basis of the EPS you use (annual, TTM, FW, et al). Despite the variance, these commonly quoted P/E does not reflect the true economic earning power.

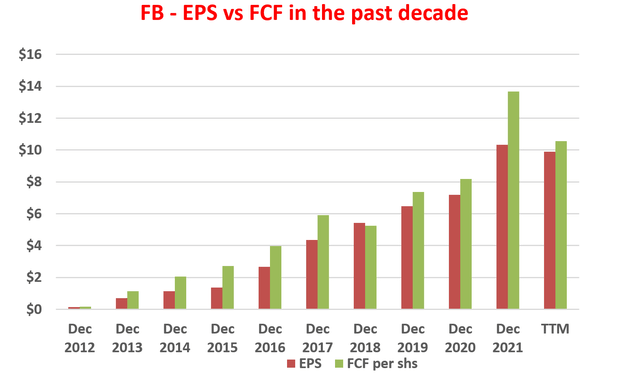

You can already see the discrepancy by simply looking at the free cash flow (“FCF”) and EPS comparison shown in the following chart. You can see that its FCF has been consistently higher than EPS. As a result, its FCF-earnings conversion ratio has been consistently and substantially above 1. In recent years since 2018, its FCF-earnings conversation ratio is on average 121% and fluctuates only within a narrow range from about 98% to 132%. In the next section, we will see that the FCF underestimates the true owners' earnings too because ALL CAPEX expenses have been considered a cost in the calculation of FCF.

Author based on Seeking Alpha data

FB’s growth CAPEX and owners' earnings

As detailed in my earlier article, the key to understanding the OE is to distinguish between growth and maintenance CAPEX. Growth CAPEX is optional and should not be considered a cost, as best explained by the following quote from Buffett (I added the emphasis):

These represent (“a”) reported earnings plus (“b”) depreciation, depletion, amortization, and certain other non-cash charges...less (“c”) the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume...Our owner-earnings equation does not yield the deceptively precise figures provided by GAAP, since (“c”) must be a guess - and one sometimes very difficult to make. Despite this problem, we consider the owner earnings figure, not the GAAP figure, to be the relevant item for valuation purposes...All of this points up the absurdity of the 'cash flow' numbers that are often set forth in Wall Street reports. These numbers routinely include (“a”) plus (“b”) - but do not subtract (“c”).

Estimating (“c”) is indeed difficult and involves a more advanced understanding of the financial statements. This article analyzed (“c”) for FB using Bruce Greenwald’s method (detailed in my earlier article on AAPL and also Greenwald’s book entitled Value Investing).

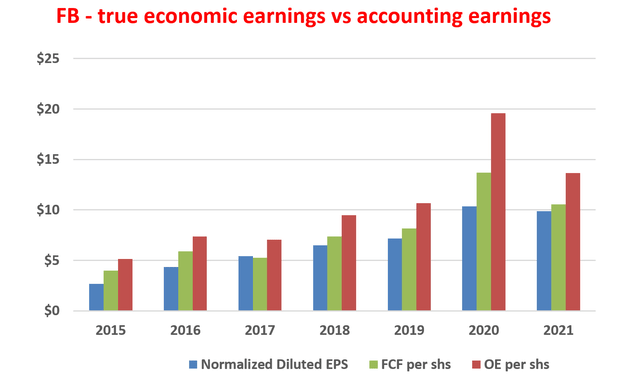

Under this background, the following chart shows FB’s true economic earnings compared to its accounting EPS and FCF in recent years. The key observations from this chart are:

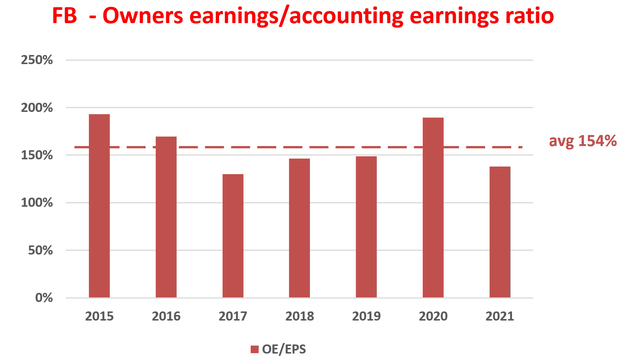

- FB’s OE is significantly higher than both its FCF and its EPS. As aforementioned, its FCF is on average 121% of its earnings. And its owners’ earnings are higher than its FCF by another 27% because a large part of the CAPEX expenditures (about 56% on average since 2018) is growth expenditures. As a result, its OE is about on average 54% higher than its accounting EPS.

- As an example, FB spent more than $33B on total CAPEX (over $18B last year and $15B in 2020). And Bruce Greenwald’s analysis shows that only about $9.5B is for the mandatory maintenance CAPEX, the rest is all for growth. To me, this is a sign of a high-growth compounder. It shows FB can employ large amounts of incremental capital to pursue new growth opportunities in areas like VR as to be elaborated more later.

Author based on Seeking Alpha data.

Author based on Seeking Alpha data.

Valuation is low and future growth is completely disregarded

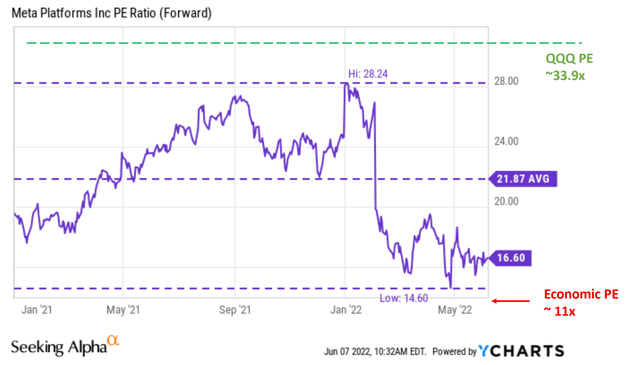

At its current price, FB’s valuation is about 16.5x FW P/E, already below its historical average and also the NASDAQ 100 index. Its forward P/E has fluctuated from a bottom of 14.6x to a peak around 28x over the past few years, with an average of 21.9x. Compared to its own historical record, the current P/E is at more than a 25% discount from the historical mean. Compared to the NASDAQ index, its P/E is only about ½ of the index. The index is valued at about 33.8x P/E (represented by the QQQ fund based on Yahoo Finance data). And as detailed above, In terms of the owners' P/E, its valuation is even lower based, only about 11x.

Seeking Alpha

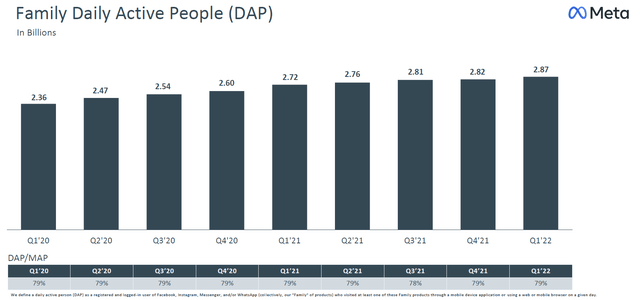

In terms of growth, its future growth has been completely disregarded. Admittedly, there are good reasons to be concerned in the short term. And its growth may be muted for the next few quarters. Management announced disappointing guidance for the first quarter and slower user acquisition. Many headwinds caused the negatives and are likely to persist, such as inflation, supply-chain disruptions, and privacy changes to Apple’s iOS system that prevent advertisers from tracking users without their consent. All told, it is experiencing difficulties to monetize. Its average price per ad decreased by 8% YOY. Although on the bright side, active users are still growing. For example, family daily active people (“DAP”) increased from 2.82 a quarter ago to 2.87 in the past quarter.

FB earnings report

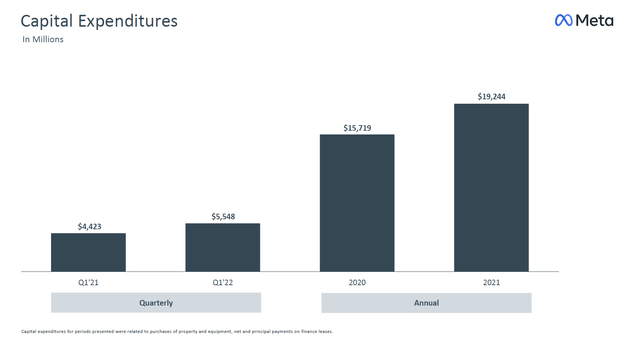

Looking past these short-term issues, the business is well-positioned for growth in the long term. it generates strong cash to fund its CAPEX expenditures and future products. CAPEX expenditures were $5.55 billion for the first quarter of 2022, an ~25% increase from $4.4 billion last year. And as aforementioned, the majority of the expenditures are growth CAPEX to support future growth areas. And there are key areas that FB is investing in as CEO Mark Zuckerberg commented (abridged and the emphasis were added by me). The company remains well-positioned in the social media space. I see active users continue to increase to support its existing segments, while investment in new technologies such as AI and VR presents plenty of upside catalysts.

I think it's useful to level-set on our business trajectory over the last few years. After the start of COVID, the acceleration of e-commerce led to outsized revenue growth, but we're now seeing that trend back off. However, based on the strong revenue growth we saw in 2021, we kicked off a number of multi-year projects to accelerate some of our longer-term investments, especially in our AI infrastructure, business platform, and Reality Labs.

FB earnings report

Final thoughts and risks

FB is currently a growth stock priced as a terminally stagnating stock. Its accounting P/E is only about 16x and owners' earnings P/E is only 11x. All negatives have been fully priced in, and I view these negatives as only temporary. Positive catalysts are completely disregarded including the renormalization of supply-chain at advertisers, its active user growth, and its future products in AI and VR.

Finally, risks. Besides the near-term headwinds mentioned above, FB faces a few other risks. FB faces market demand renormalization risk. As the CEO commented, COVID unexpectedly accelerated the penetration of e-commerce. But now that acceleration is leveling off. The company may have over-expanded in the past a few years (like many other companies during a long bull run and epic QEs from the Fed) and have capacity redundancy to digest as CFO Dave Wehner commented (the emphases were added by me):

In closing, our advertisers are adjusting to a new digital advertising landscape brought about by recent mobile platform changes while navigating a complex set of macroeconomic challenges. Given the resulting revenue headwinds, we have adjusted our plans for hiring and expense growth this year.

Comments