The US-Iran War is Escalating—So Why Did I Just Close My Long Oil Trades?

First, let me update you on my recent trading moves. I haven't been particularly active in equities lately; instead, I've maintained a light short position on the Euro and locked in some profits from a crude oil bull calendar spread (buying the near month and selling the deferred month three months out). Currently, my dprofits are entirely concentrated in my futures account.

Today, I closed my crude oil calendar spread position, booking a modest profit over the past few days. Remember our trading rule? "Rest during minor volatility, rest during extreme volatility, and no rest when there is no volatility". When a major risk event triggers massive market swings, our best approach in the futures market is to minimize our trade frequency, increase our win rate, and appropriately reduce our position sizing. In event-driven markets, the volatility is simply too extreme, and taking on such outsized risks in futures is a poor risk-to-reward proposition.

BUT, why did I close out the calendar spread on crude oil?

On one hand, crude oil has already approached its previous resistance high. The upward momentum has decelerated, and the overbought RSI indicator suggests a potential top and subsequent pullback.

On the other hand, as Morgan Stanley previously projected, a one-month blockade of the Strait of Hormuz should price in a 15% premium over pre-conflict levels. A rough calculation puts this 15% "war premium" right around the $80 mark. Any move beyond that would exceed the anticipated premium cost of a one-month supply disruption.

Most importantly, WTI crude has already broken through the 33% seasonal rally threshold I previously outlined. Having achieved this target, we are now entering what I warned about in my last update: the $74 to $80 zone is an area of heavy selling pressure. Pushing higher will invite aggressive selling, which is why I recommended capturing short-term upside profits via a bull calendar spread.

Historical Screenshot Reference

回顾:为什么特朗普这次不再TACO,美以对伊发动战争想得到什么?(原油行情要大爆发?)

$美国原油ETF(USO)$ $WTI原油主连 2604(CLmain)$ $小原油主连 2604(QMmain)$ $WTI原油2604(CL2604)$ $微型WTI原油主连 2604(MCLmain)$

My previous forecast has now played out perfectly.

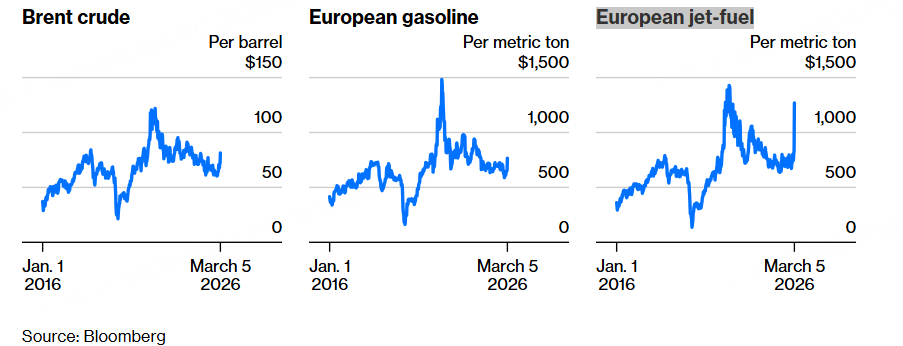

Furthermore, based on our observations, while The prospects of the US-Iran war are becoming increasingly unclear,and the war between the US/Israel and Iran is intensifying, we are 7 days in, and I see no signs of either side backing down. Yet, despite this, sentiment in the energy markets has not spiraled out of control. Take a look: aside from a moderate uptick in crude oil and a modest rise in European gasoline, only heating oil has shown a sharp, vertical 90-degree surge.

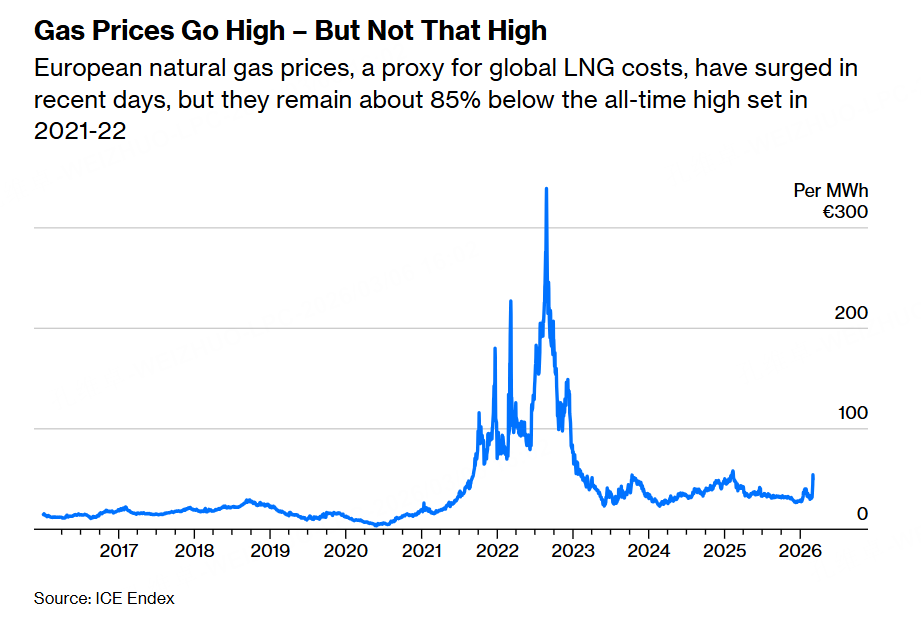

Additionally, European natural gas prices remain relatively subdued, showing little reaction compared to the dramatic spikes seen in 2021 and 2022.

$两倍做多彭博天然气ETF-ProShares(BOIL)$ $两倍做空彭博天然气ETF-ProShares(KOLD)$ $天然气主连 2604(NGmain)$

Likewise, coal prices in both China and the US remain at normal levels. A market dynamic where a single sensitive energy asset surges while all other related energy commodities remain calm clearly indicates a lack of widespread panic. It shows that energy inventories are still sufficient and the market is not pricing in a conflict lasting longer than a month.

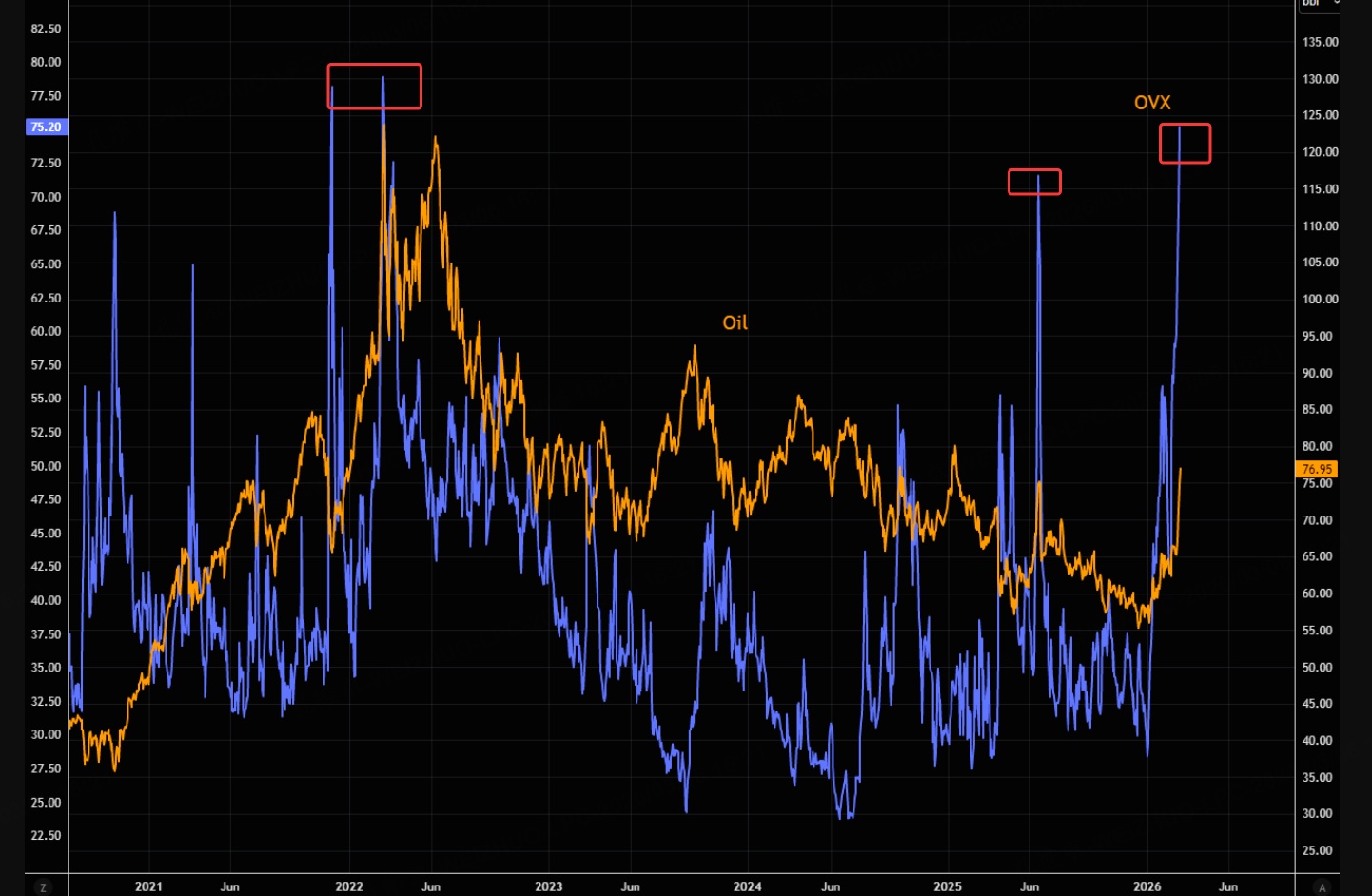

Moreover, in the short term, the implied volatility (VIX equivalent) for US crude oil has hit historical highs, making further upside bets unjustifiable.

$标普500波动率指数(VIX)$ $波动率短期期货指数ETF(VIXY)$ $1.5倍做多短期期货恐慌指数ETF-Proshares(UVXY)$

Therefore, I decided to close out the hedged bull calendar spread first. I will observe how WTI performs above $80 before deciding whether to chase the rally

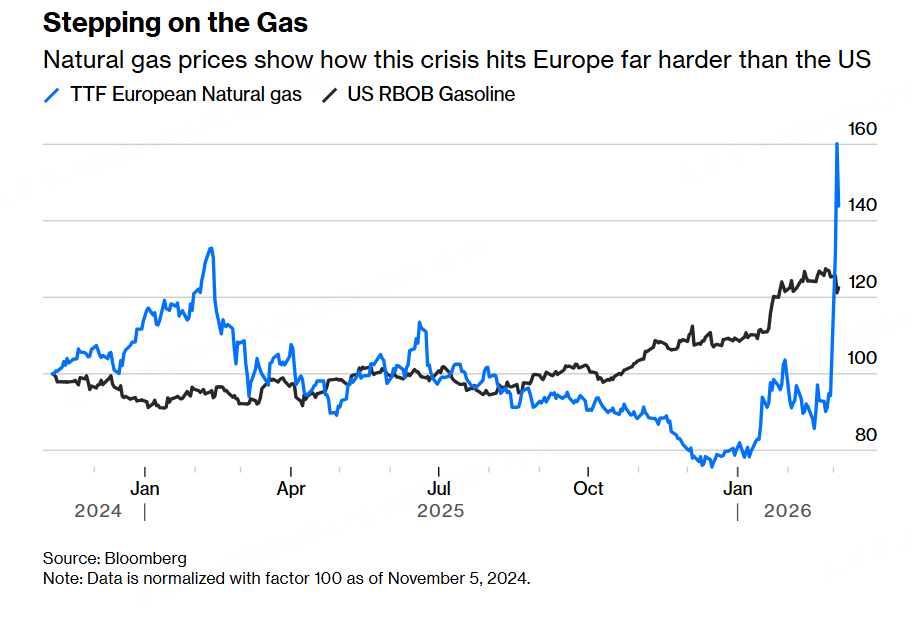

As the war enters deeper waters, the financial markets' reaction suggests that not only have US markets avoided significant damage, but they have actually benefited. Looking at short-term natural gas prices, the surge in Europe has notably outpaced that in the US, where energy prices remain much calmer.

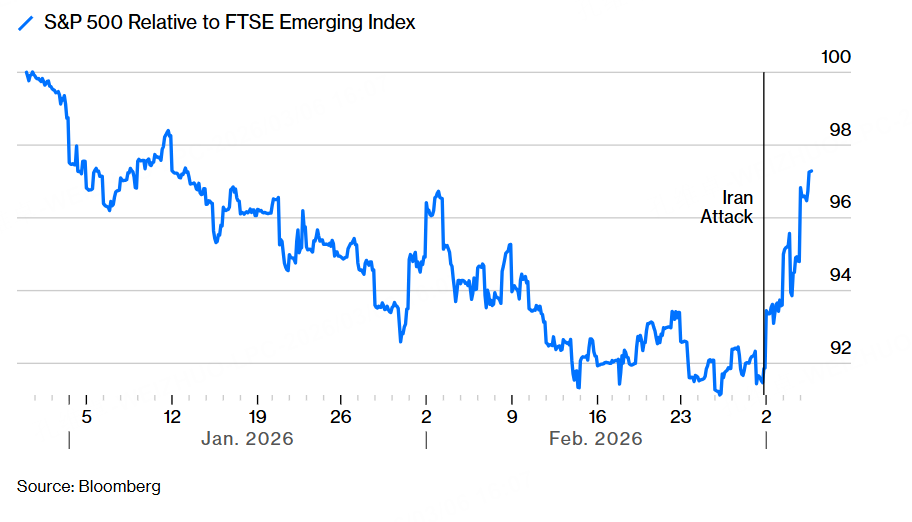

Since the outbreak of the war, market capital has actually dumped massive amounts of emerging market equities to chase US stocks, bringing back the outperformance of US equities relative to emerging markets.

$SP500指数主连 2603(ESmain)$ $道琼斯指数主连 2603(YMmain)$ $NQ100指数主连 2603(NQmain)$

This is genuinely bad news for Iran, as it demonstrates the significant resilience of Trump's wartime economy. If he decides to be bolder and deploys ground troops to force a regime change in Iran, the outlook for Tehran appears rather bleak. If Trump successfully secures a war-driven regime change in Iran before the election, the likelihood of a Republican victory will increase substantially. And as the probability of war escalation and a prolonged conflict grows, the US Dollar Index continues to climb—an overarching positive for dollar-denominated assets.

$美元ETF-PowerShares DB(UUP)$ $欧元主连 2603(EURmain)$ $新兴市场美元债ETF-iShares(EMB)$

In summary, out of the projected one month, only 7 days have passed. This war-driven market action has a long way to go. Let's wait and see.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.