Is the Oil Rally Running Out of Steam? Is It Time to Go Long U.S. Equities?

Global financial markets have recently grown increasingly complex, and it is evident that market capital is currently undergoing a drastic risk repricing. Against this backdrop, both commodities and equity markets are exhibiting signs of exhaustion, struggling to sustain their recent trajectories. Crude oil may be facing fading upward momentum, while US equities—battered by capital outflows and suppressed by rising yields—appear vulnerable to further weakness at any moment.

Short Bets Intensify on US Equities

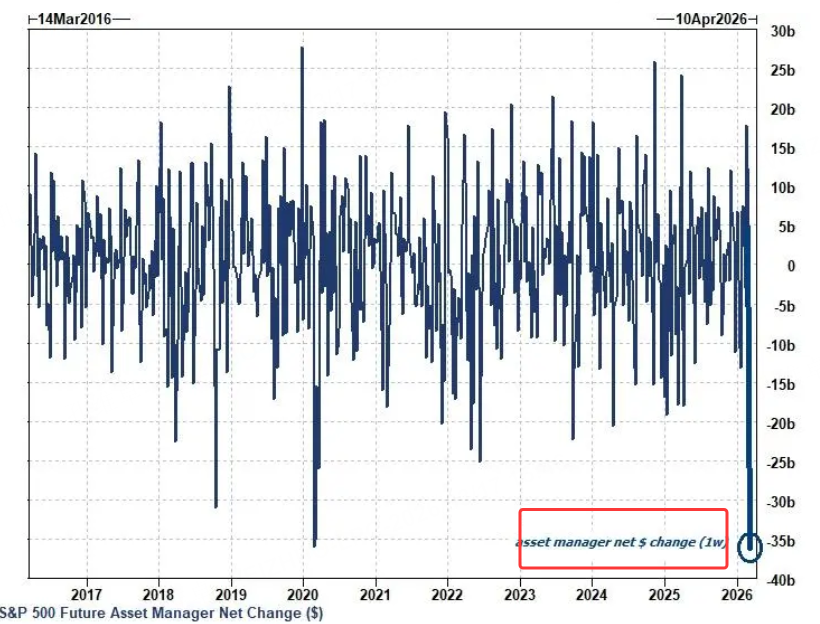

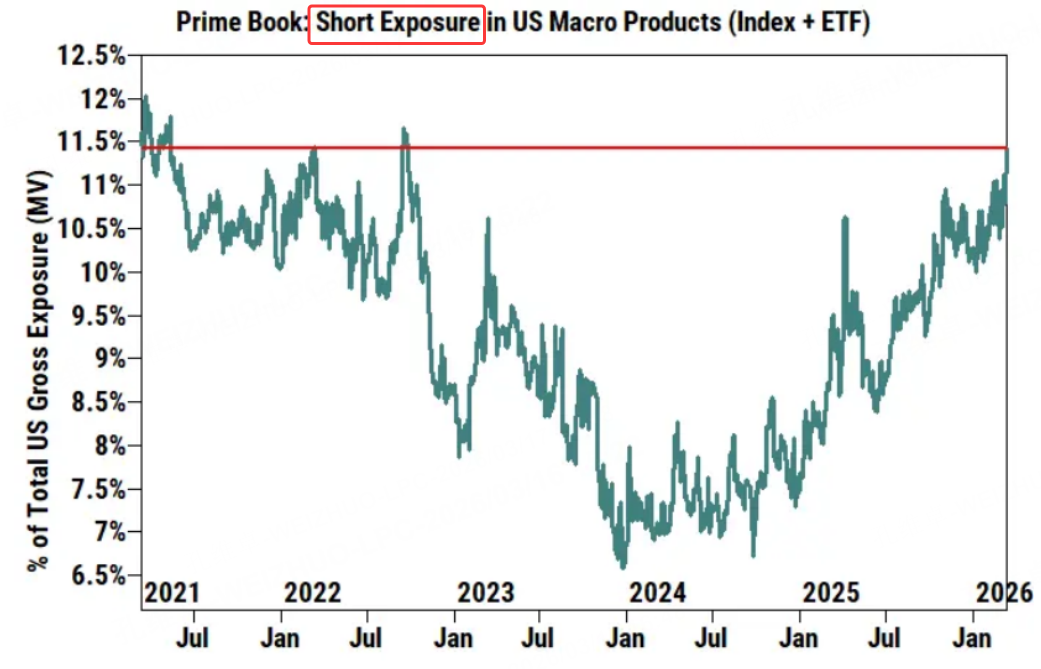

Institutional trading desk data reveals that the selling pressure on US equities is not to be underestimated. Goldman Sachs' Prime Book data flashes a distinctively negative signal: US equities have faced sell-offs for the fourth consecutive week. More alarmingly, hedge funds are not only selling but actively increasing their exposure to short products, while asset managers have offloaded a record volume of S&P futures.

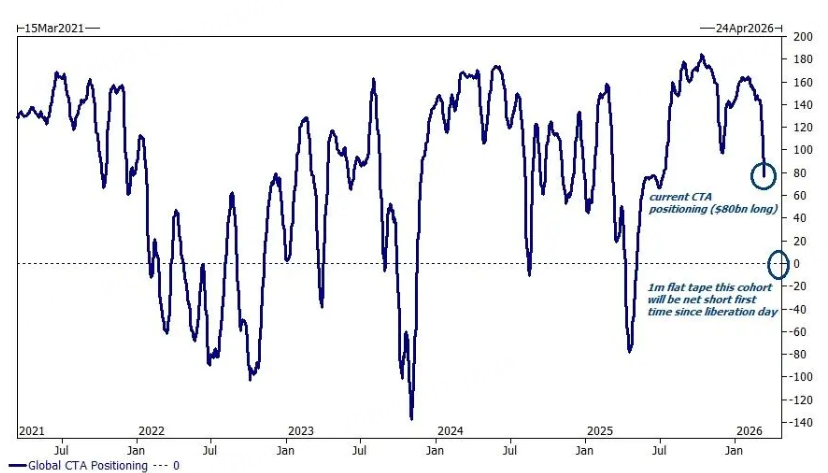

In terms of trend-following strategies, CTA (Commodity Trading Advisor) funds are now definitively in sell mode. Over the past week, CTAs have executed massive position liquidations, cutting roughly $50 billion. According to Goldman Sachs' quantitative models, an estimated $69 billion worth of assets will be sold over the next week, a figure that could soar to $98 billion over the coming month.

Resonance Risk of Option Structures

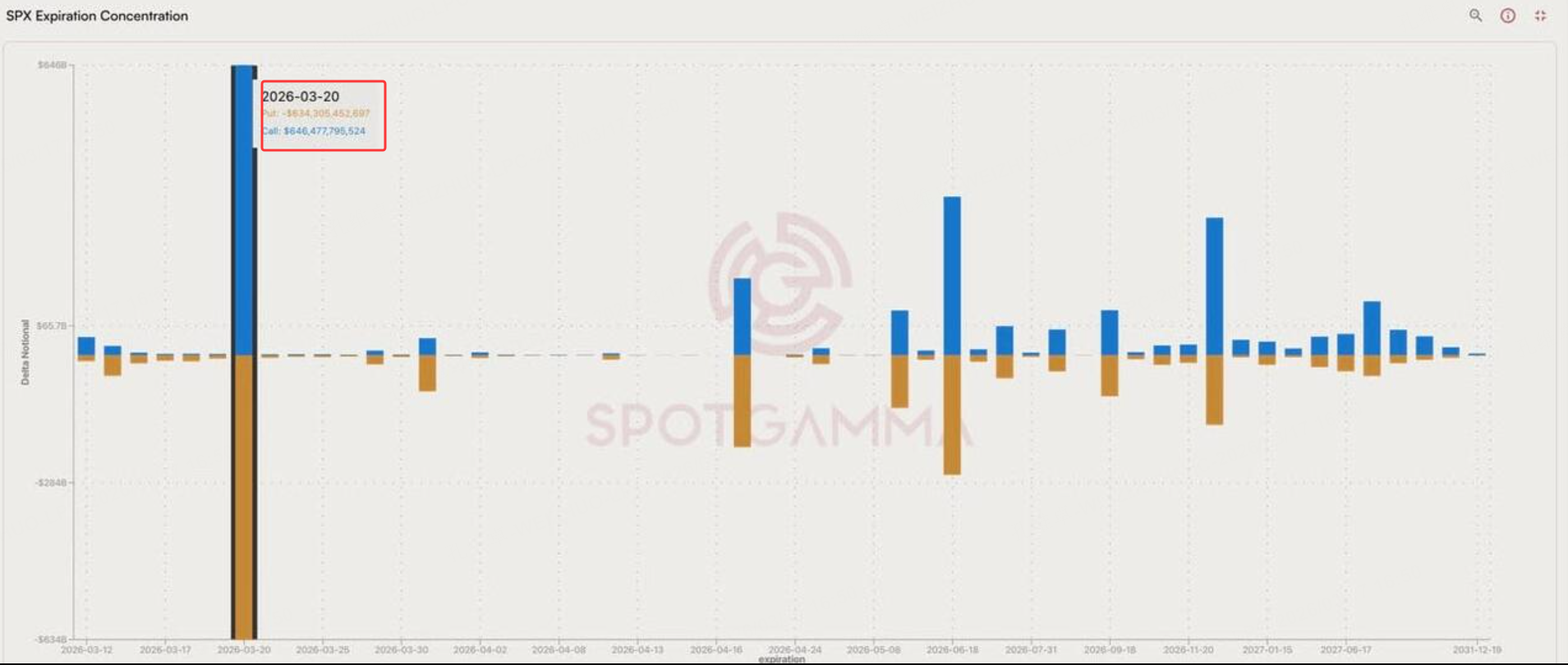

Another core driver of US equity vulnerability stems from the expiration risks of key structural option positions. Particular attention must be paid to JPMorgan's massive collar option portfolio. This quarter, the portfolio holds a staggering 35,000 S&P 500 put option spread contracts, coupled with the simultaneous sale of call options at a 7,155 strike price.

This colossal option structure is slated to expire at the end of March. Upon expiration, it is highly predictable that dealers will inevitably need to reposition their portfolios to hedge against risks, which will exert a significant impact on the market. Consequently, the quarterly option expiration on March 31 (OPEX, also known as "Triple Witching Day") will serve as an exceptionally critical juncture. Compounded by the Federal Reserve's FOMC meeting on March 18, these two major events could act as potent amplifiers of market volatility.

Meanwhile, the global liquidity environment is visibly tightening at a rapid pace. Over the past two weeks, the GS Global FCI (Goldman Sachs Global Financial Conditions Index) has spiked by more than 50 basis points. This marks the most aggressive tightening trend since August 2023, representing a magnitude exceptionally rare outside of crisis periods.

On the yield front, the 10-year US Treasury yield faces the risk of a technical breakout. There are currently two upside resistance levels at 4.4% and 4.6%. Should the 4.4% threshold be breached, it is highly probable to test the 4.6% high.

If the 30-year US Treasury yield breaches the 5% red line, the Federal Reserve will be forced into countermeasures. Prior to that point, the selling pressure on US equities will be heavy enough to very likely trigger an accelerated sell-off. This is precisely why utilizing the VIX or equity index put options for downside protection remains absolutely essential until the current macroeconomic turbulence subsides.

Crude Oil Rally Shows Exhaustion

Currently, the trajectory of the S&P 500 index displays a highly synchronized correlation with crude oil. This indirectly underscores that inflation expectations driven by crude oil prices remain the core factor weighing on equity indices. During several historical oil crises (such as in 1974, 1980, 1990, and 2022), the S&P 500 declined by an average of roughly 12% when oil prices spiked, with a median maximum drawdown of approximately 23%. Although the United States' reliance on foreign energy has substantially decreased today, a stagflationary environment will nonetheless drive capital out of momentum-heavy sectors like technology and redirect it toward defensive sectors such as energy and healthcare. The recent drawdowns in the Goldman Sachs Hedge Fund VIP basket and the broad-based declines across US fundamental hedge funds perfectly align with this historical pattern.

However, while crude oil currently acts as the "primary menace" to US equities, its own upward momentum may no longer be sustainable. At present, crude oil prices are 50 percentage points above the fair value projected by institutions. Although not yet at historical extremes, this is already the second-highest deviation level on record. If the previous surge to $120 marked the peak of this current wave of volatility, then as the deviation widens, it is highly probable that oil will transition into a phase of peaking and retracing.

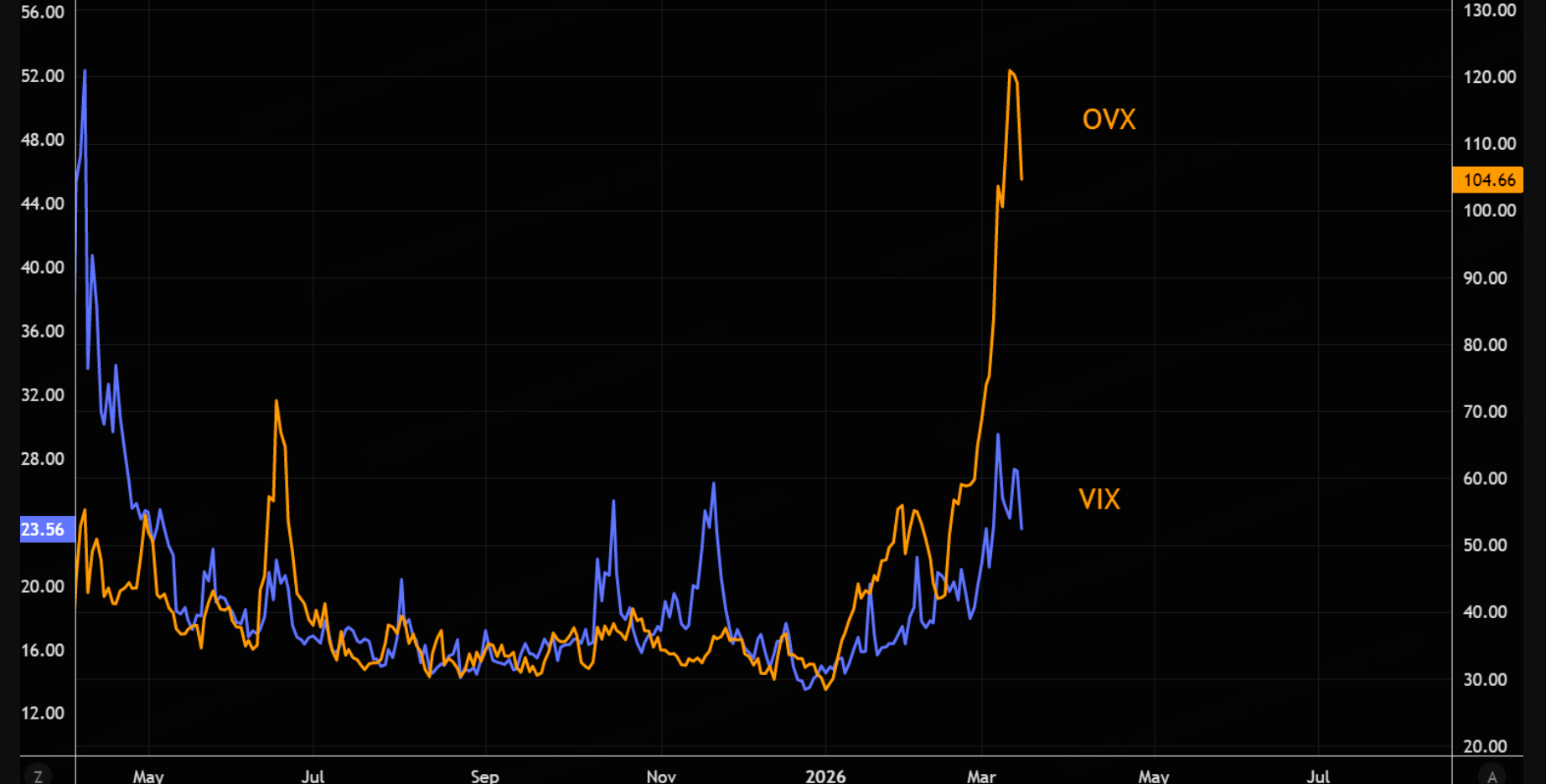

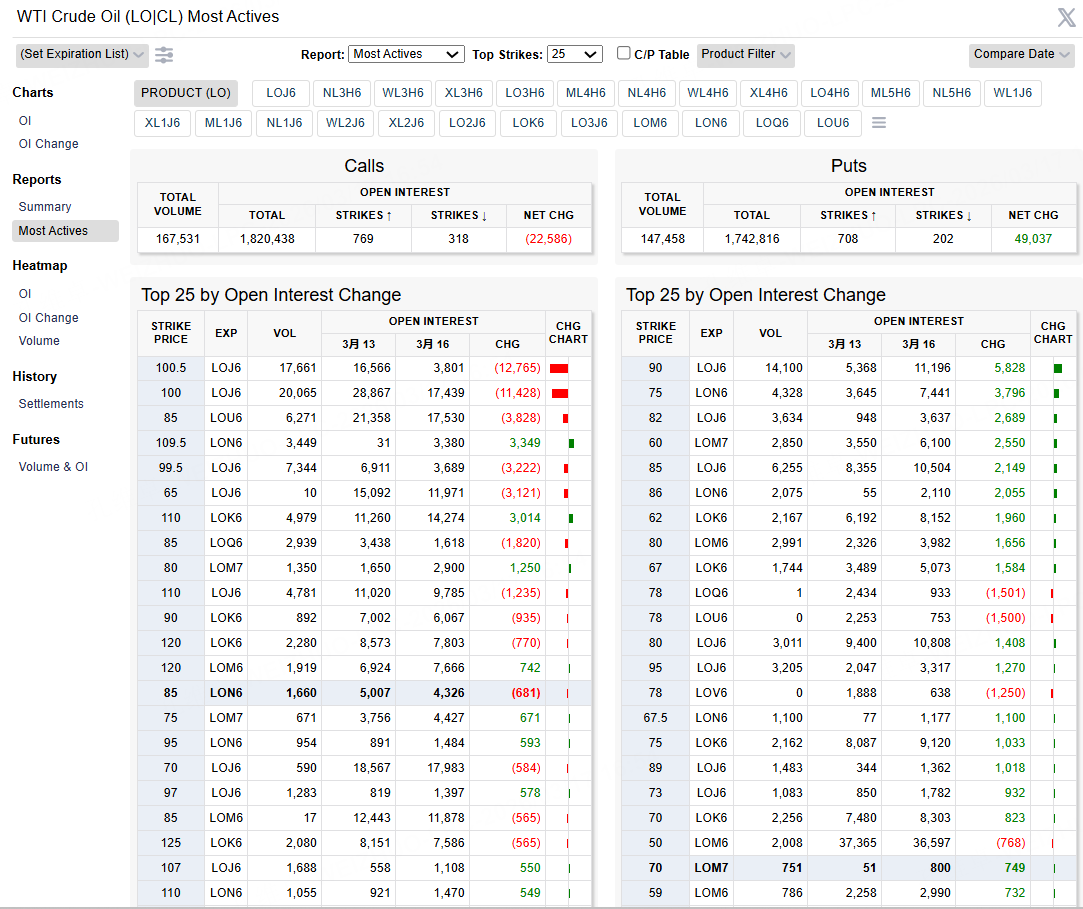

Furthermore, the crude oil volatility index (OVX) has already exhibited an inverted V-shaped reversal. Judging from the volume distribution of WTI crude oil futures options, massive option block trades on March 16 were primarily concentrated in deep out-of-the-money (OTM) options. The major call option blocks were primarily betting on the $109 level (slightly above the $107 resistance); meanwhile, the major put option blocks were densely clustered at $75, $80, and $90, with the largest OTM put order placed at $90. This indicates that the implied selling strategies within the options market assume oil prices are unlikely to substantially break above $109 in the near term, with the anticipated short-term downside floor situated around $90.

Conclusion

Synthesizing capital flows, the intensity of macroeconomic tightening, and options market bets, the capital exodus from US equities is far from over. The trading volume distribution of equity index futures options indicates that the market's expected downside magnitude remains substantial. Meanwhile, crude oil—acting as the root source of inflation—despite still suppressing US equities in the short term, is exhibiting signs of exhausted upward momentum across its technicals, fair value deviation, and derivatives pricing. Therefore, we conclude that the current crude oil rally is likely to decelerate, while US equity indices may continue to weaken. Investors must remain highly vigilant regarding future market volatility

$NQ100指数主连 2606(NQmain)$ $SP500指数主连 2606(ESmain)$ $道琼斯指数主连 2606(YMmain)$ $黄金主连 2604(GCmain)$ $白银主连 2605(SImain)$ $WTI原油主连 2605(CLmain)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- PhoebeReade·03-17Oil rally fading fast, equities shaky. [看跌]1Report