Alcoa's 20% Five-Day Rally: A Deep Dive into the "Big Five" Aluminum Majors' Fundamentals

A Geopolitical Supply Shock Spurs 20% Sector Weekly Rally

Executive Summary for SG Investors

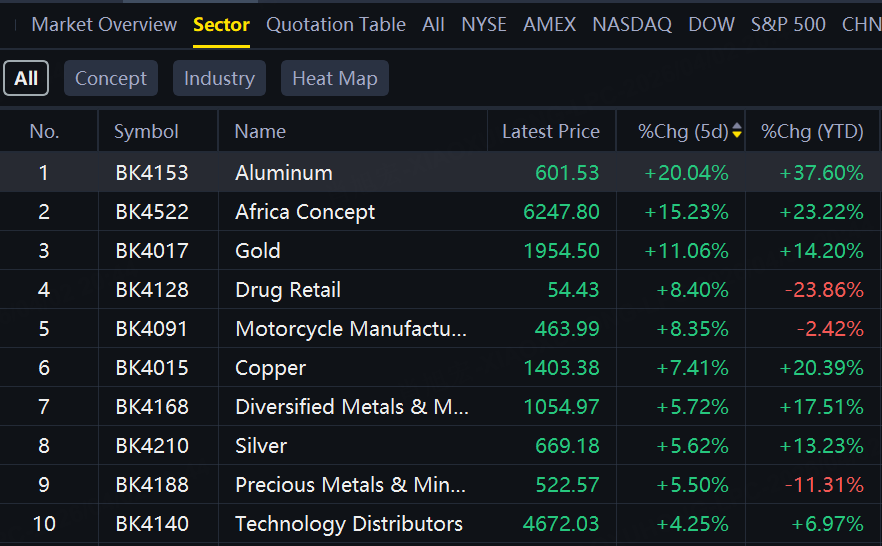

The U.S. aluminum sector has emerged as the top-performing industry cluster this week, with the five primary listed names gaining +37.6% sector-wide year-to-date.

The catalyst: a perfect storm of Middle East supply disruptions (Iranian missile strikes on GCC smelters) and aggressive U.S. tariff protectionism creating a structural deficit in global aluminum markets.

Key Catalysts Driving the Rally

1. Middle East Supply Crisis (Primary Driver)

On March 28, 2026, Iranian missile strikes targeted the Gulf's largest aluminum smelters—UAE's Emirates Global Aluminium (EGA) and Bahrain's Alba—causing "significant damage" and operational halts.

Supply Impact:

-

Regional Risk: The Middle East accounts for ~9% of global aluminum output (~6.8M tonnes capacity), with 80-85% designated for export.

-

Deficit Projection: Wood Mackenzie forecasts a 3.0–3.5M tonne global supply shortfall in 2026.

-

Price Action: LME Aluminum futures surged to $3,492/tonne (4-year high), with spot prices jumping +6% in a single session.

-

Chokepoint Risk: The Strait of Hormuz facilitates ~60% of bauxite feedstock for regional smelters; prolonged conflict threatens sustained supply constraints.

2. U.S. Tariff Escalation & Industrial Policy

The Trump administration is advancing a "full-value" 25% tariff regime on finished aluminum products (replacing the current 50% duty on metal content only).

Investment Implications:

-

Domestic Price Premium: U.S. Midwest Premium has already breached $1.00/lb, creating a structurally higher pricing environment for domestic producers.

-

Import Substitution: U.S. smelters gain pricing power versus Chinese and Russian imports.

-

Fiscal Impact: Projected to generate ~$70B in tariff revenue over 10 years.

3. Structural Demand Tailwinds

Global inventories hover at multi-decade lows, while demand accelerates from:

-

AI Infrastructure: Data center construction requiring electrical-grade aluminum

-

EV & Energy Storage: Battery enclosures and grid infrastructure

-

Defense Spending: Aerospace and military-grade aluminum alloys

Company-Specific Analysis: The "Big Five" U.S. Aluminum Plays

|

Rank |

Ticker |

Market Cap |

5-Day Return |

Core Business Model |

Supply/Demand Sensitivity |

SG Investor Notes |

|---|---|---|---|---|---|---|

|

1 |

$19.0B |

+22.76% |

Global Alumina Leader |

Very High: Pure-play aluminum leverage to LME prices. Alumina shortage provides additional margin expansion. Alumina business acts as natural hedge against aluminum price volatility. |

USD Commodity Proxy: Direct exposure to Western industrial policy. Consider forex hedge if SGD/USD volatility concerns. |

|

|

2 |

$6.3B |

+26.54% |

U.S. Primary Smelter Leader |

Highest: Pure-play primary smelter with full U.S. production base. Maximum beneficiary of Midwest Premium pricing. Energy cost volatility (natural gas) is the key risk factor. |

High Beta Play: Most leveraged to U.S. tariff policy. Glencore relationship provides offtake certainty but introduces counterparty concentration. |

|

|

3 |

$3.7B |

+7.10% |

High-Value Added Specialist |

Moderate: Downstream processor—benefits from aerospace backlog but faces input cost pressure. Defense contracts provide stability. Lower rally reflects margin compression concerns from raw material inflation. |

European Exposure: HQ'd in France; offers EU-U.S. arbitrage exposure. Aerospace cycle hedge for SG portfolios. |

|

|

4 |

$2.1B |

+10.82% |

Specialty Aluminum Expert |

Moderate-High: Focus on high-margin specialty products with strong pricing power. Aerospace order backlogs extend 2-3 years. Defense demand is acyclical; able to pass through raw material costs. |

Quality Factor: Lower volatility than commodity producers. Suitable for income-focused SG investors seeking industrial exposure with defensive characteristics. |

|

|

5 |

$286M |

+6.62% |

Diversified Manufacturer |

Low: Diversified revenue base; aluminum extrusion is non-core. Smallest market cap and weakest rally reflects skepticism about margin resilience amid input cost inflation. |

Micro-Cap Speculation: Liquidity risk for institutional SG investors. Better suited for high-risk retail exposure. |

Investment Thesis & Risk Framework

Short-Term (1–3 Months)

-

Catalyst: Geopolitical risk premium in aluminum prices.

-

Top Picks: $Century Aluminum(CENX)$ (highest torque to U.S. premiums) and $Alcoa(AA)$ (alumina shortage beneficiary).

Medium-Term (6–12 Months)

-

Catalyst: Structural deficit supported by U.S. industrial policy and energy transition demand.

-

Allocation: Overweight primary producers (AA, CENX); underweight downstream processors (CSTM, TG) until margin stabilization.

Key Risks for SG Investors

-

USD/SGD Volatility: Commodity plays are USD-denominated; SGD appreciation could erode returns.

-

China Supply Response: If Chinese smelters ramp production (violating capacity caps), global prices could collapse.

-

Global Recession: Prolonged Mideast conflict could trigger demand destruction in manufacturing.

-

Energy Cost Inflation: European and U.S. smelters remain vulnerable to natural gas/electricity price spikes.

Bottom Line

For Singapore investors seeking non-correlated, hard-asset exposure with a geopolitical alpha component, the U.S. aluminum sector offers a compelling tactical opportunity. Alcoa (AA) and Century Aluminum (CENX) represent the purest plays on the current supply shock, while Kaiser Aluminum (KALU) offers a defensive, specialty-materials alternative with aerospace/defense tailwinds.

Recommendation: Overweight the sector with a 6–12 month horizon; monitor LME inventory levels and Gulf shipping lane security as key risk indicators.

For SG users only, Welcome to open a CBA today and enjoy access to a trading limit of up to SGD 20,000 with unlimited trading on SG, HK, and US stocks, as well as ETFs.

🎉Cash Boost Account Now Supports 35,000+ Stocks & ETFs – Greater Flexibility Now

Find out more here.

Complete your first Cash Boost Account trade with a trade amount of ≥ SGD1000* to get SGD 688 stock vouchers*! The trade can be executed using any payment type available under the Cash Boost Account: Cash, CPF, SRS, or CDP.

Other helpful links:

-

💰Join the TB Contra Telegram Group to Get $10 Trading Vouchers Now🎉

-

How to open a CBA. How to link your CDP account. Other FAQs on CBA. Cash Boost Account Website.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.