TSMC's Q3 Preview: AI Momentum Fuels Robust Outlook Amid Capacity Constraints

As $Taiwan Semiconductor Manufacturing(TSM)$ approaches its October 16 earnings release, investors are positioning for upbeat signals on artificial intelligence uptake and supply bottlenecks in advanced nodes and advanced packaging. Analysts anticipate the company will project fourth-quarter sales holding steady from the prior period, elevating full-year 2025 dollar-based expansion to the mid-30% zone—far surpassing earlier projections. Management is poised to express optimism regarding data center AI traction, highlighting persistent shortages in 3nm/2nm fabrication and CoWoS through 2026, without delving into next year's formal forecasts or spending plans just yet. Expect reaffirmation of Arizona facility timelines, alongside dismissal of any Intel collaboration rumors, whether funding or partnerships. Profit margins should hit the upper guidance boundary, buoyed by elevated orders and currency tailwinds that counterbalance startup expenses at new sites.

September figures exceeded forecasts marginally, with monthly output dipping 1% sequentially yet surging 31% annually, pushing quarterly totals to NT$990 billion—a 6% quarter-over-quarter and 30% year-over-year advance. This topped internal models and aligned with the top of the dollar-denominated range (US$31.8-33 billion). iPhone 16 production acceleration and AI surge propelled over 100% utilization in 3nm and 5nm lines. Margins are forecasted near 57.3%, within the 55.5-57.5% band (at NT$29/USD), aided by a 4% quarterly new Taiwan dollar slide and premium-node strength.

Looking to the final quarter, sales should stabilize quarter-on-quarter, contrasting two prior expansions, thanks to data center AI vigor, iPhone momentum, and node scarcity. Android handset and gadget sectors may linger soft, improving on initial downside hints (high-single-digit drop) and matching broader views. Margins could sustain 57-58%, navigating Arizona scaling and 2nm preliminaries, supported by revenue steadiness and softer local currency.

Capital outlays for 2025 are set to hover at US$38-42 billion (midpoint US$40.5 billion), constrained by immediate cleanroom limits, with a sharp 19% year-on-year climb to US$48 billion in 2026 from 2nm rollout, CoWoS scaling, and Arizona phase two acceleration. Formal 2026 guidance likely defers to January.

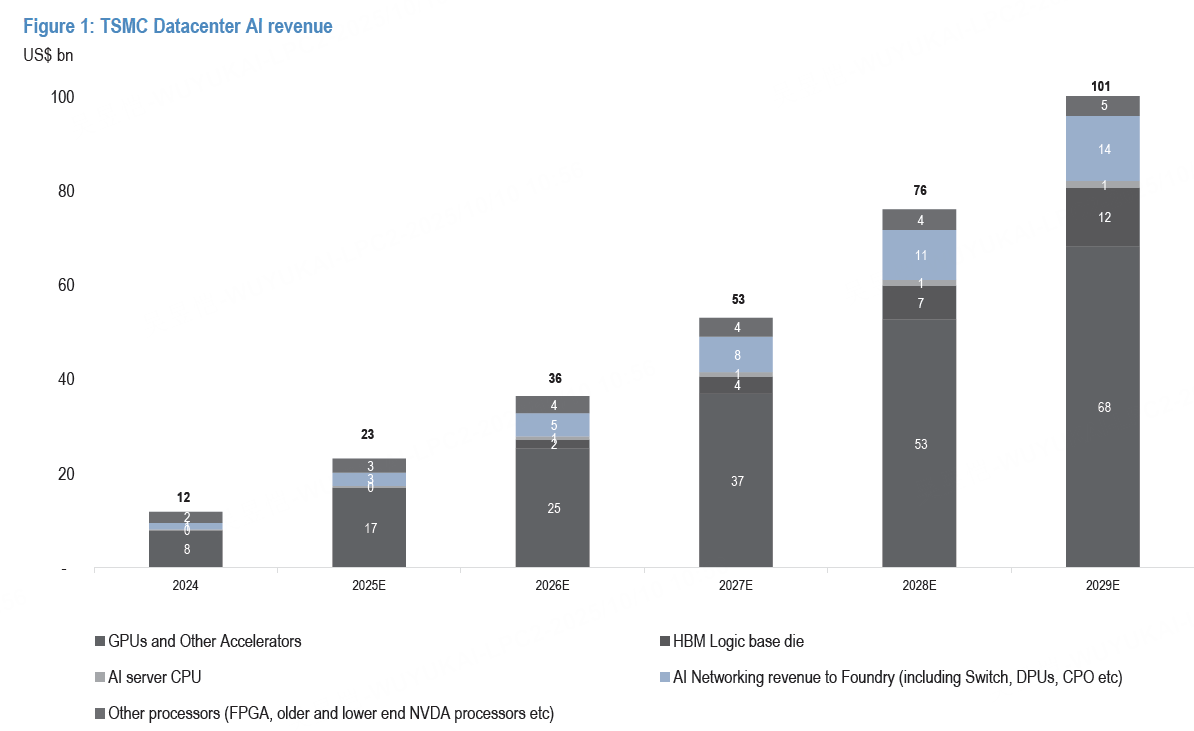

AI narrative stays aggressively positive: Post-upward revisions, hyperscaler pacts (e.g., OpenAI-Nvidia-Oracle) and cloud provider signals point to compute hunger persisting into 2026. Datacenter AI sales are modeled at 53% compound annual growth through 2029 (versus prior mid-40s%), spanning GPUs, custom chips, interconnects, and HBM foundations—though no refresh expected this cycle. CoWoS output expands 60%, drawing from key partners like Broadcom, Nvidia, and AMD, with incrementally brighter 2026 tones. Yet 3nm emerges as the primary chokepoint, as accelerators shift nodes; checks suggest Nvidia's Rubin uses flip-chip over CoWoS.

Advanced-node pressures and mitigation strategies: 5nm/3nm/2nm output stays constrained into 2026. Acceleration eyed for 3nm via Arizona phase two shifts (early 2026) and Fab 18 reallocations from 5nm, plus potential 7nm-to-4nm swaps in Taichung amid idle capacity since mid-2022. 2nm pacing commentary gains urgency with handset/high-performance computing pull from 2027, amplified by recent hyperscaler boosts—spotlighting expansion rhetoric.

Stateside growth and Intel ties: Arizona phase two revenue kicks off 2027 (moves mid-2026), phase three for 2nm follows in 2027, addressing U.S. client needs, duties, and policy nudges. Ecosystem immaturity caps quicker ramps for cutting-edge tech. Leadership should underscore disinterest in Intel alliances or equity grabs.

Categary | 2024 | 2025E | 2026E | 2027E | 2028E | 2029E |

GPUs & Accelerators | 8 | 17 | 25 | 37 | 53 | 68 |

HBM Logic Base Die | 2 | 4 | 7 | 12 | 23 | 36 |

AI Server CPU | 0 | 0 | 1 | 1 | 1 | 1 |

AI Networking (to Foundry) | 1 | 3 | 5 | 8 | 11 | 14 |

Other Processors | 2 | 3 | 4 | 4 | 4 | 5 |

Total Datacenter AI Revenue (US$ bn) | 13 | 27 | 42 | 62 | 92 | 124 |

Source: Firm data and projections. Note: Totals derived from stacked components; networking includes switches, DPUs, CPO.

Core Investment Case

TSMC's dominance in AI chips and edge inference underpins enduring expansion, via superior nodes (3nm/2nm) and packaging prowess. Dollar sales could hit mid-20% in 2026, extending into 2027, propelled by data center AI (50%+ compound rate 2024-2029 from Nvidia/custom chips, plus networking/HBM), with CoWoS scarcity lingering. Margins hold high-50s via steady currency, moderated U.S. drag, node premium adjustments, and node demand. At 20x forward earnings to mid-2026, the target exceeds five-year norms, baking in 3nm gains and 2nm acceleration.

Key Headwinds

Tariff shocks or worldwide slowdowns.

AI softening beyond 2026.

Accelerated U.S. sites eroding margins more than projected.

Riding TSMC's AI Wave: Why Capacity Crunch Makes It a Must-Hold into 2026

Straight talk: If you're not overweight TSMC right now, you're missing the semiconductor gold rush. With shares at NT$1,440 and my June 2026 target at NT$1,550 (20x forward P/E), the setup screams upside—driven by insatiable AI hunger that's turning fabs into bottlenecks faster than Nvidia can ship GPUs. Forget the noise on consumer softness; data centers are the real story, and TSMC's lock on advanced nodes means pricing power and margin resilience ahead.

The AI Engine That's Just Revving Up

September sales clocked NT$331 billion (down 1% month-on-month, up 31% year-on-year), capping Q3 at NT$990 billion—6% quarter-on-quarter pop that beat whispers and nailed the high end of guidance. Credit iPhone 16 ramps and AI's turbocharge: 3nm/5nm utilization north of 100%. Margins? Expect 57%+ (top of 55.5-57.5% band), as TWD weakness (~4% quarter-to-date) offsets Arizona growing pains.

Q4 holds flat sequentially—way better than the mid-single-digit dip once floated—thanks to AI/datacenter firepower and iPhone continuity, even as Android lags. Full-year dollar growth? Mid-30s, with capex steady at US$40 billion midpoint. But 2026? Brace for 19% spending surge to US$48 billion on 2nm/CoWoS/Arizona phase two. No formal guide yet—that's January—but qualitative vibes will scream bullish.

Datacenter AI alone? JPM models 53% CAGR to 2029 (US$13 billion in 2024 to US$124 billion), stacking GPUs (Nvidia/customs), HBM dies, server CPUs, networking (switches/DPUs), and more. Hyperscalers like OpenAI/Oracle are slamming doors for 2026 compute; CoWoS jumps 60% on Broadcom/Nvidia/AMD demand. Bottleneck shifts to 3nm as Rubin skips CoWoS for flip-chip—meaning TSMC hikes prices without mercy.

Capacity Plays: No Room at the Inn

Leading-edge (5/3/2nm) stays slammed through 2026. Watch for 3nm fast-tracks: Arizona phase two moves early next year, Fab 18 flips 5nm space, Taichung eyes 7-to-4nm swaps amid idles. 2nm commentary? Critical, with smartphones/HPC pulling hard into 2027—OpenAI upside just sweetened the pot.

U.S. buildout accelerates (phase two revenue 2027, phase three 2nm moves then), chasing clients/duties/policy. But ecosystem youth caps speed for elite processes. Intel? TSMC waves it off—no stakes, no ventures.

Valuation: Premium for a Monopoly

At 20x to mid-2026, it's a stretch over historicals—but justified by 23.5% revenue growth (versus street 20%) and 6% EPS edge. Risks? Tariffs/slowdown bite, AI hype fades post-2026, or U.S. ramps dilute margins quicker. Still, structural moat in AI accelerators/edge (N3/N2 roadmap, packaging lead) points to mid-20% 2026 sales, high-50s gross margins on steady TWD, tame U.S. bleed, and node hikes.

Bottom line: TSMC isn't just riding AI—it's engineering the rails. Accumulate on dips; this train leaves the station in 2026.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Valerie Archibald·2025-10-10TOPA little tough to buy now in that it raises my average cost, but I am a true believer that a year from now, people will be kicking themselves for not buying TSM while it was under $300!1Report

- Mortimer Arthur·2025-10-10Just saw the news from Taiwan. TSMC ready to do volume production of 2 nm chips before the end of the year.1Report

- SiliconTracker·2025-10-10TSMC's AI lead is unstoppable - fabs printing money with these chip shortagesLikeReport

- OYoung·2025-10-10Exciting journey aheadLikeReport